There’s a season for all things, the Good Book tells us. But if you’re the CEO of a company valued under $2 billion, we understand why you might have been experiencing a crisis of faith lately. But now, the time of redemption – of your stock appreciation rights at least – is at hand.

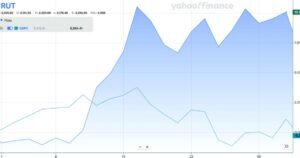

Small stocks, as measured by the Russell 2000 index, have struggled for years to keep up with the S&P 500, its better-known, large-cap counterpart. Over the past five years, the S&P returned more than 80% to investors, while the Russell eked out less than half of that.

But if we zero in just on the month of July …

… we see a most dissimilar picture. Small-caps gained more than 10% in a month, while large-caps actually lost a little ground, not assuming dividends.

Both indices have given back a little in the volatile first week of August, but still: Why all of a sudden are small caps roaring? And how long will it last?

The same, only different

According to CME Group, the two stock averages tend to correlate over time but diverge over the course of an economic cycle. That is, if you’d put $1,000 in an S&P index fund and another $1,000 in a Russell index fund 40 years ago, your results would be comparable. But if you put all of it into the S&P as the economy expanded then rotated it into the Russell when a recession was looming, you might look like a stock-picking genius.

Small-caps outperformed during the unsettled times in the late 1970s and early 1980s, then during the 1990-91 recession, and again during the turbulent first decade of the 21st century, when we got hit with shock after shock: the dotcom implosion, 9/11, the financial crisis and whatever else. The Russell also had a moment during the Covid pandemic but, oddly enough, not during the recessionary part of it. From October 2020 through March 2021, as things started to get back to normal, small-caps surged but, by the end of the year, the large-caps caught up.

Maybe we’re focused too much on raw returns, though, when we ought to be considering the risk of investing in small stocks as well. Small-cap stocks are inherently riskier than large-caps, so investors should expect to be awarded with superior rather than equal returns. And that’s one major reason why hedge funds and institutional investors tend to ignore the Russell components.

The case for small-caps today

Another reason that Russell stocks had been underperforming is that they tend to be low-tech. The Industrial, Financial Services, Health Care and Consumer Discretionary sectors comprise more than half of the index’s value. Barely 10% of it is invested in Information Technology.

But now that investors are rotating out of Tech, the ball is bouncing toward the Russell.

And of course, there’s that macroeconomic specter that casts a shadow over every company in the market: interest rates. Big companies have much easier access to bank financing and can float fixed-income bonds if they need even more money. As a result, large-caps’ capital stacks are heavily weighted toward fixed-income debt. Small caps, though, don’t have that luxury.

“Approximately 1/3 of the Russell 2000 are financed with floating rates, compared to only 6% of companies in the S&P 500,” according to BlackRock.

With interest rates on the cusp of dropping – quickly, many believe – the capital access playing field might be leveling off and the degree of risk for investing in small-caps might be dialing down.

Time to play small-ball?

Predictions about where the Russell 2000 goes from here are all over the place. Well, not all over the place. For instance, we won’t make any here. Still, there are indicators that the outlook for small-caps hasn’t been this good in years.

“For small cap stocks to significantly rally, a couple of things are needed in the coming weeks and months: continued U.S. economic growth and Federal Reserve interest rate cuts,” according to Benzinga, a financial news website. “With these in place, investors could enter the market at attractive valuations.”

Those are also the two elements of a soft landing, which we may be experiencing right now.